The Company may also incorporate industry-accepted valuation methodologies, such as an income approach and market approach. The income approach derives fair value based on the present value of cash flows that a business or security is expected to generate in the future. The market approach relies upon valuations for comparable public companies, transactions or assets, and includes making judgments about which companies, transactions or assets are comparable. A blend of approaches may be used to determine an estimate of fair value;

| (2) | securities, loans or other assets traded on an exchange are valued generally at the official closing price or the last reported sale price on the exchange or over-the-counter market that is the primary market for such security, or if no sales or closing prices are reported, based on the mean of the last available bid and ask quotation on the exchange, market or quotes obtained from a quotation reporting system, established market makers or pricing services; |

| (3) | certain securities or assets for which market quotations or other market-based valuation methods are not readily available may be valued with reference to other securities or indices; and |

| (4) | other valuation methods, as needed. |

Where valuations are not provided by an independent source, the Administrative Agent may consult with and may ultimately rely entirely on the Operating Manager or its affiliates in determining the value of Company’s assets, although the Administrative Agent is not required to do so. The Company may engage one or more independent valuation firms to provide assurance regarding the reasonableness of a valuation for an asset that does not have a readily-available market price as of the relevant measurement date. In cases where the Company engages an independent valuation firm to value or review valuations of assets, the cost of such valuation firm is expected to be borne by the Company.

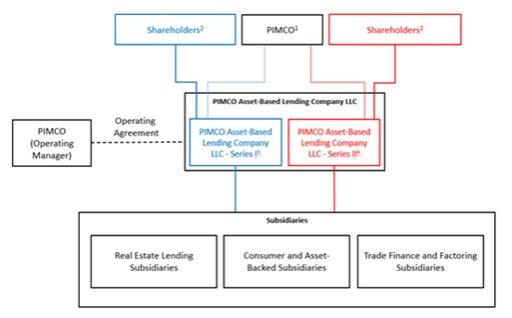

Our Structure

The following is a summary chart of our corporate structure. This chart is a simplified version of our structure and does not include all legal entities in the structure.

| 1 | As of the date hereof, PIMCO GP LXXXII, LLC holds all of 80 V Shares, which are non-economic shares that have certain rights and privileges, including the exclusive right to appoint and remove directors of the Board. V Shares are held only by PIMCO GP LXXXII, LLC and/or its affiliates, and are not being offered to other investors. |

| 2 | Certain third-party investors in the private offering hold certain Class of Shares offered for anchor investors. |

| 3 | Series I has elected to be treated as a corporation for U.S. tax purposes. |

| 4 | Series II has elected to be treated as a partnership for U.S. tax purposes. |

13